Your retirement account is not just a tax deferral vehicle.

→ For some clients, it is a tax planning opportunity hiding in plain sight.

→ Most never see it.

The Problem With the Default Tax Assumption

Roll it to an IRA.

- Not because it is always the right answer. Not because anyone modeled the alternatives. Not because the advisor ran the numbers.

- Because it is the default.

- The default works well enough for most situations.

- But for a participant who has spent a career accumulating highly appreciated employer stock inside a qualified plan, the default can cost more than half a million dollars in unnecessary federal tax — on a single account, in a single decision.

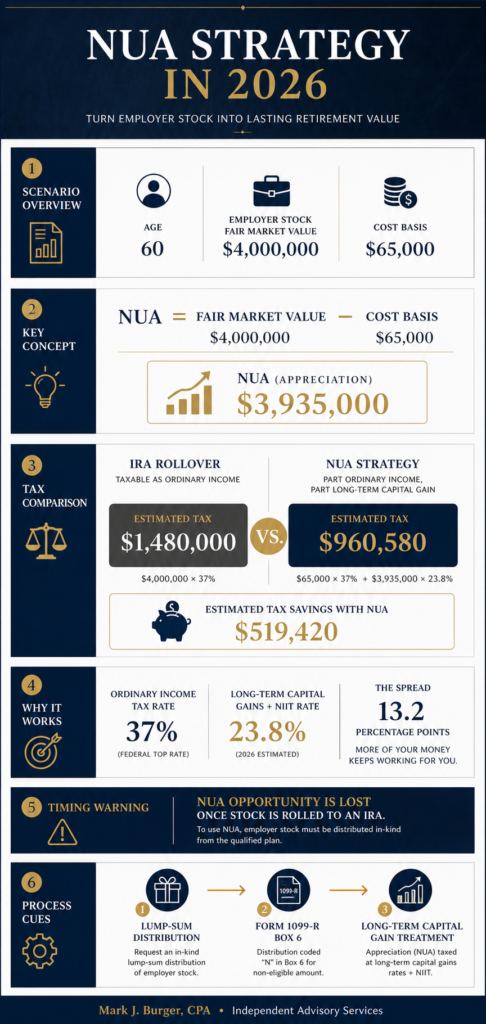

The strategy is called Net Unrealized Appreciation — NUA — and after 37 years in CPA practice, I continue to see it overlooked at precisely the moment it matters most.

What NUA Actually Is

Net Unrealized Appreciation is the difference between two numbers.

- The cost basis of employer stock inside the plan — what the plan paid for those shares over time.

- The fair market value of that stock at the time of distribution.

The gap between those two numbers is the NUA.

That gap, under the right conditions, is taxed at long-term capital gains rates rather than ordinary income rates.

That distinction is not minor. In 2026, a taxpayer in the 37% ordinary income bracket faces a maximum long-term capital gains rate of 20%. Add the 3.8% Net Investment Income Tax that applies at this income level, and the effective rate on the NUA becomes 23.8%.

The spread between 37% and 23.8% is 13.2 percentage points.

When a $4,000,000 stock position carries a cost basis of $65,000, that spread applies to 98.4% of the account balance.

The Mechanics: What Actually Happens

The participant takes a lump-sum distribution of employer stock from the qualified plan — not a rollover, not a partial withdrawal — within a single tax year following a qualifying triggering event.

Triggering events include:

- Separation from service

- Reaching age 59½

- Death of the plan participant

- Disability, for self-employed individuals

A participant who retires at age 60 satisfies the separation from service trigger. Importantly, the 10% early withdrawal penalty does not apply. Under IRC Section 72(t)(2)(A)(v), participants who separate from service in the year they reach age 55 or later are exempt. At age 60, the penalty does not enter the analysis.

The distribution is reported on Form 1099-R. The cost basis flows into Box 2a and is recognized as ordinary income in the year of distribution. The NUA appears in Box 6 and is excluded from ordinary income at that time.

When the stock is eventually sold, the NUA is reported on Schedule D as a long-term capital gain — regardless of how long the participant held the stock after taking the distribution. That long-term treatment is locked in at the time of the original distribution.

The Numbers in Practice: A 2026 Illustration

A participant retires at age 60 in 2026. The employer stock inside the plan has a cost basis of $65,000 accumulated over a career. The fair market value at the time of distribution is $4,000,000. The NUA is $3,935,000 — representing 98.4% of the total account value.

This is not a hypothetical extreme. A long-tenured employee at a publicly traded company who participated in an employer stock program for 25 to 30 years, with consistent contributions and sustained appreciation, arrives at this position.

| IRA Rollover | NUA Strategy | |

| Cost basis tax | $1,480,000 (full balance at 37%) | $24,050 (basis only at 37%) |

| NUA tax | Included above | $936,530 ($3,935,000 at 23.8%) |

| Total federal tax | $1,480,000 | $960,580 |

| Effective rate | 37.0% | 24.0% |

| Federal tax savings | — | $519,420 |

On a single account. On a single decision made at the point of retirement. Before state tax considerations. Before planning around the timing of the sale.

That is not a rounding error.

The 2026 Rate Environment Makes This More Compelling, Not Less

The One Big Beautiful Bill Act, signed into law in July 2025, permanently extended the TCJA ordinary income tax structure. In 2026, the top ordinary income rate remains at 37% applying to taxable income above $640,600 for single filers and $768,600 for married couples filing jointly.

The long-term capital gains rates for 2026 remain at 0%, 15%, and 20%. The 20% rate applies above $545,500 for single filers and $613,700 for married couples filing jointly.

For a taxpayer with $4,000,000 in employer stock, the 20% rate and the 3.8% NIIT are both certain. The combined 23.8% rate on the NUA is not a best-case outcome. It is the rate. And it is now permanent under current law.

When the Strategy Makes Sense — and When It Does Not

The NUA transaction is not universally appropriate. The analysis requires precision, not assumption.

The strategy is most compelling when:

- The cost basis is extremely low relative to fair market value — at $65,000 against $4,000,000, the basis represents 1.6% of the account value

- The participant is in the 37% ordinary income bracket and will be subject to the 20% LTCG rate plus 3.8% NIIT

- The participant is age 55 or older at separation, eliminating the 10% early withdrawal penalty on the cost basis

- The employer stock represents the dominant asset inside the plan

Risks that belong in every NUA conversation:

- Concentration risk — a $4,000,000 single-stock position held outside the plan is significant undiversified exposure

- State tax conformity — California, New Jersey, New York, Oregon, and Minnesota tax capital gains as ordinary income at the state level, partially offsetting the federal advantage

- NIIT — the 3.8% Net Investment Income Tax on the NUA at sale is already incorporated into the 23.8% effective rate; it is not optional at this income level

- IRMAA — recognizing $3,935,000 of capital gain in the sale year places the taxpayer in the top IRMAA tier, increasing Medicare Part B and Part D premiums for the two years following; this is a cost of the strategy, not a reason to avoid it. You can avoid the IRMMA by strategically selling the stock as you diversify the investment.

- Irreversibility — once the lump-sum distribution is taken, it cannot be undone

The Planning Failure Is Not Ignorance. It Is Timing.

- The NUA strategy requires action at a specific moment — the distribution event.

- Once the stock is rolled to an IRA, the opportunity is gone.

- There is no corrective amendment. There is no amended return. There is no going back.

- For the participant described above, that means a permanent, unrecoverable loss of $519,420 in federal tax savings. Not a planning opportunity missed. A tax liability created that did not have to exist.

- The barrier is not complexity.

- It is the absence of an independent advisor at the right moment.

What a Proper NUA Analysis Requires

A complete NUA analysis involves more than comparing two tax rates. It requires modeling the full tax impact across both the distribution year and the anticipated sale year.

- What is the marginal ordinary income rate in the distribution year, inclusive of the cost basis recognition?

- What is the combined long-term capital gains and NIIT rate on the NUA at the anticipated sale?

- Does the participant qualify for the age 55 separation exemption from the 10% early withdrawal penalty?

- What is the state’s treatment of the NUA — ordinary income or capital gains?

- What is the IRMAA impact in the two years following the sale year, and does a phased sale reduce that burden meaningfully?

- What is the concentration risk profile, and what is the plan for diversification after the distribution?

These questions require the client’s actual numbers. The analysis that surfaces the right answer is not available from the plan administrator. It is not available from the rollover paperwork.

It is available from an independent CPA who has no interest in which vehicle receives the assets.

The Principle Behind the Strategy

Tax planning is not about finding loopholes.

It is about understanding the structure of the law well enough to apply it correctly when the circumstances align.

The NUA provision has existed in the tax code for decades. It is not obscure. It is not aggressive. It is a legitimate mechanism that Congress built into the framework of qualified plan distributions.

For a participant retiring at 60 with $4,000,000 of appreciated employer stock, the cost of not knowing about it is $519,420.

That number is not abstract.

It is the difference between what the law requires and what the default produces.

The sooner this analysis is done, the more options remain available.

Wait long enough, and the default decision has already been made.

37 years advising employers and business owners. Independent perspective. No product relationships. No rollover incentives. Contact Mark J Burger CPA

To learn more about Mark J Burger CPA

- Does my state conform to federal NUA treatment? It depends entirely on where you live. States fall into three categories. No income tax states — Florida, Texas, Nevada, Wyoming, Washington, South Dakota, Tennessee, and Alaska — preserve the federal savings in full. The 23.8% combined rate is your complete burden. States that tax capital gains as ordinary income — California (13.3%), New Jersey (10.75%), New York (10.9% state, up to 14.8% combined with New York City), Oregon (9.9%), and Minnesota (9.85%) do not recognize the federal capital gains preference. The NUA is taxed at the state ordinary rate on top of the 23.8% federal rate. In California, the combined burden on the NUA approaches 37%. The strategy still beats a full IRA rollover on a combined basis, but the margin narrows significantly. Most other states conform to the federal preferential treatment. The federal advantage carries through to the state return largely intact. One important exception worth knowing: Pennsylvania generally does not tax retirement income from qualified plans for residents over age 59½. A Pennsylvania resident who qualifies may owe no state tax on either the cost basis or the NUA sale — which amplifies the federal savings further.

- How do I find out what my cost basis is, and who do I ask? The plan recordkeeper — the financial institution that administers your 401(k) maintains the cost basis. Do not ask for your account value or your statement. Ask specifically for the aggregate cost basis of the employer stock that would appear in Box 2a of Form 1099-R in the event of a lump-sum distribution and ask for the NUA amount that would appear in Box 6. Put the request in writing. Keep the response. Two complications arise regularly. First, if your employer has changed recordkeepers over the years, historical basis records may have been transferred imperfectly. Second, older plans with paper-based records may require manual reconstruction. Neither problem makes the strategy unavailable, but both require resolution before the distribution is taken — not after. Request the number at least six to twelve months before any anticipated separation or retirement date. An incorrect basis figure cannot be corrected once the distribution paperwork is executed.

- After I take the NUA distribution, when should I sell the stock? The NUA itself — $247,500 in the base illustration — is taxed at 23.8% whenever you sell. That does not change based on timing. It was locked in at the distribution date. What timing does affect is any appreciation or depreciation that occurs after the distribution. If the stock rises after the distribution and you sell within 12 months, the new gain is taxed as ordinary income at 37%. If you wait past 12 months from the distribution date, the new gain is taxed as long-term capital gains at 23.8%. On a $25,000 post-distribution gain, that difference is $3,300 in additional federal tax. Not enormous — but avoidable with patience. If the stock falls after the distribution, the NUA tax obligation does not shrink. It was fixed at the distribution-date value. The post-distribution loss becomes a capital loss — usable against other gains or up to $3,000 per year against ordinary income — but it does not reduce what you owe on the NUA. This is the concentration risk that makes a defined diversification plan essential from the start. The other timing consideration most people miss is IRMAA. The year you sell the stock, the NUA gain appears as income on your tax return. Medicare uses income from two years prior to set premiums. A $247,500 gain in 2026 affects your 2028 Medicare premiums. If the position can be sold in two portions across two tax years, the IRMAA surcharge may be reduced. Whether that is worth the continued concentration risk is a judgment call that requires modeling your specific income in both years.

This post is provided for educational purposes and does not constitute tax advice specific to your situation. Consult your CPA or tax advisor before taking any action with respect to qualified plan distributions.